What Can Indian Investors Learn from Market Leaders That Have Survived Multiple RBI Rate Cycles?

What Can Indian Investors Learn from Market Leaders That Have Survived Multiple RBI Rate Cycles?

Indian market leaders that have navigated multiple RBI interest-rate cycles reveal enduring lessons in balance-sheet discipline, pricing power, capital allocation, and risk management. Studying these companies helps investors identify businesses capable of compounding returns across both tightening and easing monetary phases.

Thank you for reading this post, don't forget to subscribe!Introduction: Why RBI Rate Cycles Matter for Investors

Interest rates set by the Reserve Bank of India (RBI) influence borrowing costs, consumption, capital investment, and asset valuations across the economy. Over the last two decades, India has witnessed multiple rate-hiking and rate-cutting cycles, driven by inflation control, growth support, global shocks, and currency stability.

Yet, while many companies struggle during these transitions, a handful of market leaders continue to grow earnings, protect margins, and strengthen competitive positions. For retail investors, understanding what these survivors do differently can significantly improve long-term portfolio outcomes.

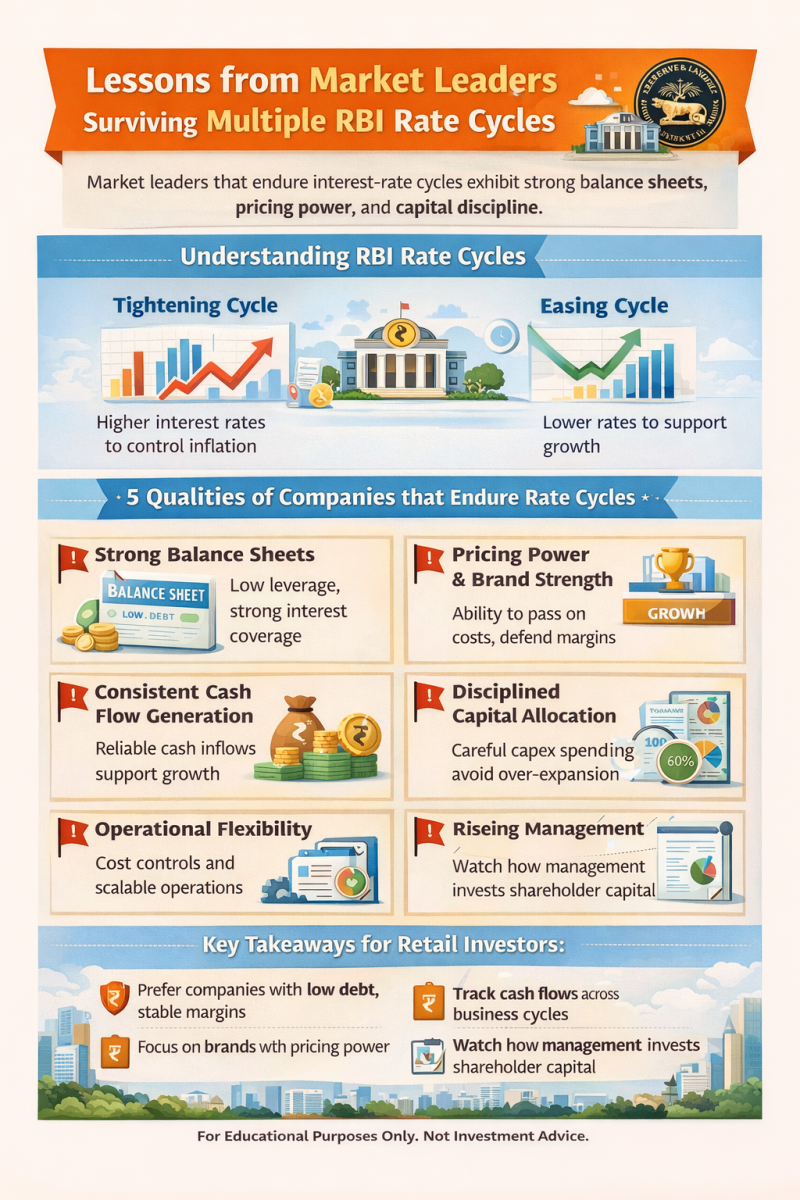

Understanding RBI Rate Cycles in Simple Terms

RBI rate cycles broadly fall into two phases:

-

Tightening cycles: Higher interest rates to control inflation

-

Easing cycles: Lower rates to stimulate growth and credit demand

Each phase affects companies differently:

-

Higher rates increase interest costs and pressure valuations

-

Lower rates boost borrowing but can compress margins through competition

Market leaders are not immune — but they adapt better.

Source (RBI – Monetary Policy Framework):

https://rbi.org.in/commonman/English/scripts/commpol.aspx

Key Traits of Companies That Survive Multiple Rate Cycles

1. Strong Balance Sheets and Conservative Leverage

Companies that endure rate hikes typically maintain:

-

Low debt-to-equity ratios

-

High interest coverage

-

Ample liquidity

Lower leverage cushions profitability when borrowing costs rise.

Investor takeaway: Avoid businesses that rely on cheap credit for survival.

2. Pricing Power and Brand Strength

Market leaders often possess:

-

Strong brands

-

Dominant market share

-

Differentiated products

This allows them to pass on higher costs to customers without destroying demand — a critical advantage during tightening cycles.

3. Consistent Cash Flow Generation

Cash-generating businesses manage:

-

Capex without excessive borrowing

-

Working capital efficiently

-

Dividend payouts and reinvestment prudently

Cash flows reduce dependence on external financing during volatile rate environments.

4. Disciplined Capital Allocation

Survivors avoid over-expansion during easy money phases and instead:

-

Invest selectively

-

Prioritise return on capital employed (ROCE)

-

Avoid value-destructive acquisitions

Capital discipline becomes visible only across multiple cycles.

5. Operational Flexibility

Market leaders often show:

-

Cost control mechanisms

-

Variable cost structures

-

Ability to scale production up or down

This flexibility protects margins when demand weakens due to higher rates.

India-Focused Case Studies: Companies That Endured RBI Rate Cycles

Case Study 1: HDFC Bank

Why it stands out:

HDFC Bank has successfully navigated multiple tightening and easing cycles through:

-

Conservative credit underwriting

-

High CASA (low-cost deposits) ratio

-

Stable net interest margins

Even during rising rate phases, its asset quality remained resilient.

Source (HDFC Bank Investor Relations):

https://www.hdfcbank.com/about-us/investor-relations

Case Study 2: Asian Paints

Why it stands out:

Asian Paints demonstrates how pricing power and distribution strength protect profitability:

-

Ability to pass on raw material cost increases

-

Strong brand loyalty

-

Efficient supply chain

Interest rate volatility had limited impact on long-term earnings trajectory.

Source (Asian Paints Annual Reports):

https://www.asianpaints.com/more/investors.html

Case Study 3: Tata Consultancy Services (TCS)

Why it stands out:

As a net cash company, TCS benefits from:

-

Minimal interest cost exposure

-

Strong free cash flow

-

High ROE across cycles

Rate hikes have limited direct impact, making IT leaders structurally resilient.

Source (TCS Investor Relations):

https://www.tcs.com/investor-relations

Case Study 4: Nestlé India

Why it stands out:

Nestlé India showcases defensive resilience:

-

Stable demand regardless of interest rates

-

Strong pricing power

-

Consistent margin protection

Such companies often outperform during uncertain macro phases.

Source (Nestlé India Investor Information):

https://www.nestle.in/investors

How Rate Cycles Affect Valuations — and What Leaders Do Differently

During rate hikes:

-

Valuation multiples compress

-

Debt-heavy companies suffer disproportionally

During rate cuts:

-

Over-leveraged firms temporarily benefit

-

But leaders compound steadily regardless of rate direction

Market leaders focus on earnings quality, not valuation expansion alone.

What Retail Investors Should Learn and Apply

1. Analyse Performance Across Multiple Cycles

Avoid judging companies based on one favourable phase.

2. Prefer Balance Sheet Strength Over Short-Term Growth

High ROCE and low leverage matter more than headline growth.

3. Look for Pricing Power

Margins that remain stable across cycles signal durability.

4. Avoid Rate-Sensitive Business Models

Companies surviving only due to low rates often struggle when policy tightens.

5. Track Management Behaviour

Capital allocation decisions during easy money phases reveal long-term intent.

Regulatory and Disclosure Perspective

SEBI mandates regular disclosures, including:

-

Quarterly results

-

Debt levels

-

Management commentary

These disclosures help investors assess resilience across macro cycles.

Source (SEBI – LODR Regulations):

https://www.sebi.gov.in/legal/regulations/may-2025/securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirements-regulations-2015-last-amended-on-may-01-2025-_93799.html

Key Takeaways

-

RBI rate cycles are inevitable and recurring

-

Market leaders survive through balance-sheet strength, pricing power, and discipline

-

Studying survivors offers a framework for long-term investing

-

Retail investors should prioritise durability over momentum

-

Consistency across cycles is a powerful quality filter

Sources & References

-

Reserve Bank of India – Monetary Policy Framework

https://rbi.org.in/commonman/English/scripts/commpol.aspx -

Reserve Bank of India – Policy Statements & Historical Data

https://data.rbi.org.in/#/dbie/home -

SEBI – Listing Obligations and Disclosure Requirements (LODR)

https://www.sebi.gov.in/legal/regulations/may-2025/securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirements-regulations-2015-last-amended-on-may-01-2025-_93799.html -

Company Investor Relations Pages

-

HDFC Bank: https://www.hdfcbank.com/about-us/investor-relations

-

Asian Paints: https://www.asianpaints.com/more/investors.html

-

Nestlé India: https://www.nestle.in/investors

-

Related Blogs:

Understanding Cash Flow Statements for Investors

Understanding the Income Statement: A Beginner’s Guide

How to Read a Company’s Balance Sheet Before Investing

Pricing Power: The Secret Behind Multibagger Stocks

ROE vs ROCE: Which Metric Matters More for Investors?

Evaluating Capital Expenditure (Capex) Plans Before Investing

How to Evaluate Management Quality: A Key Pillar of Smart Investing

Disclaimer: This blog post is intended for informational purposes only and should not be considered financial advice. The financial data presented is subject to change over time, and the securities mentioned are examples only and do not constitute investment recommendations. Always conduct thorough research and consult with a qualified financial advisor before making any investment decisions.

Q1. Do all companies benefit from rate cuts?

No. Weak business models may see temporary relief but struggle long term.

Q2. Are rate-insensitive stocks always expensive?

Often yes, but premium valuations reflect durability and earnings certainty.

Q3. Should investors change portfolios based on RBI policy?

Long-term investors should focus on business quality rather than short-term rate predictions.

Q4. Which sectors handle rate cycles best?

Consumer staples, IT services, and well-capitalised private banks tend to be more resilient.